Section

Navigation

Section

Navigation

9. Learning from Others

9.1

Introduction: Grouping by Business Models

:Cautionary Tales

9.2

A Start

9.3 Coins International

9.4 Fine Art Ceramics

9.5 Halberd Engineering

9.6

Ipswich Seeds

9.7 Seascape e-Art

9.8 Whisky Galore

:Case

Studies

9.9 Amazon

9.10

Andhra Pradesh

9.11 Apple iPod

9.12 Aurora Health Care

9.13

Cisco

9.14 Commerce Bancorp

9.15 Craigslist

9.16

Dell

9.17 Early Dotcom

Failures

9.18 Easy Diagnosis

9.19 eBay

9.20

Eneco

9.21 Fiat

9.22

GlaxoSmithKline

9.23 Google ads

9.24 Google services

9.25

Intel

9.26 Liquidation

9.27

Lotus

9.28 Lulu

9.29

Netflix

9.30 Nespresso

9.31

Netscape

9.32 Nitendo wii

9.33 Open Table

9.34

PayPal

9.35 Procter & Gamble

9.36 SIS Datenverarbeitung

9.37 Skype

9.38

Tesco

9.39 Twitter

9.40

Wal-mart

9.41 Zappos

9.42

Zipcar

9.34

PayPal

9.34

PayPal

PayPal is the largest and most popular of online payment systems, currently

holding more than 100 million active accounts in 25 currencies. {7} The payment system

was conceived in 1998 and the company launched as Confinity. Its electronic payments

system was first offered in 1999, and in 2000 the company was acquired by X.com Corporation.

The corporation renamed Confinity as PayPal, and made an initial stock offering on

Nasdaq in 2001. {6} Failing to make its own electronic payments system pay, {3} eBay

acquired PayPal in 2002 for US$1.5 billion. {1} PayPal headquarters are located in San Jose, California, USA, but the company also has operations in India, Ireland, Germany, Israel and China.

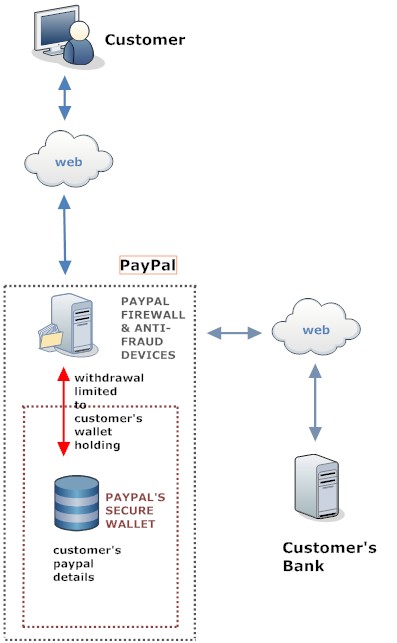

PayPal provides a secure wallet system of transferring funds for both senders and receivers. Both must open an account with PayPal and provide details of a credit, debit or bank account, which is drawn on if insufficient funds remain in the PayPal wallet ('float') to honor a transaction. Access to the account is through email address and password. {1}

PayPal is one of the great success stories of the web, and an example of first-mover advantage. In the face of stiff competition, and despite many websites set up to complain of PayPal practices, the company's net total payment volume has grown steadily, particularly from eBay purchases: US$30 billion from that source in 2008, for example, 51% of total revenues. {3} Operating income in the 2012 fiscal year was $14.07 billion up, from 11.65 billion in 2011. The net income, however, was was $2.61 billion, down from $3.23 billion in 2011.

Evolution of PayPal's Business Model

PayPal's business model went through three phases. {1}

Phase One: 1999-2000

PayPal received the bulk of its revenues from eBay purchasers who needed a cheap and easy way of making payment. Since growth was sluggish, PayPal adopted an aggressive marketing campaign, depositing $10 in new users' PayPal accounts and another $10 for each new user they recruited.

Phase Two: 2000-2002

That marketing campaign was unsustainable in the long term, and PayPal adopted the following:

1. Lowering

transaction charges to zero, hoping to earn interest on customers' floats. It failed

because customers promptly drew down their floats.

2. Bearing more of the cost

of litigation and fraud. eBay buyers using PayPal got up to $1,000 in fraud protection,

and emerchants more protection from chargebacks.

Phase Three: 2002 Onwards

After its acquisition by eBay, PayPal turned its attention to the non-eBay market, offering these terms:

1. Lowered transaction fees for high-volume merchants.

2. Recruitment

of non-eBay merchants won an increased bonus (to US$1000, up from the previous US$100

cap).

3. Persuaded credit card gateway providers to include PayPal.

4. Reduced

fees for online music purchases and other 'micropayments'.

5. Payment via text

messages on cell phones and through cloud computing. {13}

PayPal also hired a special sales force to persuade leading brands to accept PayPal, which proved successful. {9}

Swot Analysis

Strengths

PayPal became popular because of its:

1. Simplicity: opening an account can be accomplished

in a few minutes (though PayPal approval takes longer).

2. Commission charges

are modest, comparable to other Internet Payment Service providers (IPSPs) at low

transaction volumes.

3. Online merchants do not need an Online

Merchant Account, which can be difficult and/or expensive to acquire.

4. Though

still carrying the stigma of small business, PayPal is now accepted by larger companies.

{9}

5. Viral marketing: anyone receiving PayPal cash has to open an account.

Weaknesses

Loss of confidence by emerchants, who allege:

1. Being the target of many scams,

PayPal's fraud detection can be heavy-handed, freezing accounts for long periods.

{14}

2. PayPal's arbitration system is not always adhered to, hitting the emerchant

with unwarranted charge-backs.

3. Support is rudimentary: telephone, no emails,

rapid turnover in poorly-trained staff.

4. Funds drawn from a bank account cannot

be recovered (unlike credit card transactions).

5. No limit to the funds that

can be misappropriated by a PayPal transaction (again unlike credit card transactions,

which is generally restricted to $50).

6. Primitive download of e-goods: system

doesn't always work.

Opportunities

PayPal is expanding to:

1.

Accept payment via mobile text messages.

2. Be accepted in more markets: 190 in

2011.

3. Allow software companies develop applications.

4. Operate outside

the USA, notably Asia.

Threats

Threats come from increasingly sophisticated scams, litigation, and competition from other Internet Payment Service Providers.

1.

PayPal has been forced to install costly anti-fraud software (e.g. acquisition of

Fraud Sciences for $169 million in 2008), though these have proved worthwhile: losses

were $171 million in 2008, only 0.29% of total payment volume. {2}

2. Competition

comes from:

a.

Google checkout.

b. Mobile payment with Netbanx,

etc.

c. Yahoo

small business.

d. Facebook credits

system.

e.

Amazon payment services.

f.

Other IPSPs.

3. Litigation: PayPal has had to settle many claims, generally

out of court. A few sums that were disclosed: {1}

a.

Alleged violations of the Electronic Funds Transfer Act in May 2002: US$ 9.25 million

b. Failure to show clients' rights and liabilities more

accurately: US$150,000 in March 2004 to the state of New York.

c.

Illegal charging for currency conversion: PayPal and Israel Credit Cards-Cal Ltd.

paid NIS16 million in June 2011.

Points to Note

1.

Success was not immediate, but required costly marketing campaigns.

2. PayPal

has continued to see off the competition: many 'PayPal

alternatives' exist, but they have not made significant inroads.

3. PayPal

held on to its first mover advantage, but not without a struggle.

Questions

Questions

1. What is PayPal, and how does it work?

2. Describe the three phases

of PayPal growth

3. Provide a SWOT analysis for PayPal.

4. How has first

mover advantage worked for PayPal?

Sources

and Further Reading

Sources

and Further Reading

1. PayPal, Inc. Funding

Universe. Detailed account and good list of references.

2. Ecommerce 2010.

Kenneth C. Laudon and Carol Guercio Trave. Pearson 2010. 5. 64-68.

3. Case

Study: PayPal. DigitalEnterprise.

Study in extended sections.

4. PayPal case study by Axel Schultze. Axel

Schultze Blog. July 2009.

5. PayPal's Business Model by Anghel Oleg.

Slideshare. 2008. Slide show in English and Italian.

6. PayPal

Blog. Official blog site.

7. EBay/PayPal. Who we are. eBay.

Latest statistics.

8. PayPal Press Center. PayPal.

Latest financial data, etc.

9. PayPal's Business Model by Anghel Oleg.

Slide 11. Slideshare.

2008. February 2009.

10. PayPal.

Official web site.

11. Google launches Wallet service by Chris Nuttall.

FT.

September 2011. Google's answer to PayPal.

12. PayPal unveils payment system

aimed at digital goods by Geoffrey Fowler and Russell Adams. WSJ.

October 2011. Digital goods are a $16 billion-a-year industry.

13.

Your New Digital Wallet: In The Cloud But Still Tethered To Fees by Steve Henn.

NPR.

June 2012.

14. PayPal: 'Aggressive changes' coming to

frozen funds policy by Julianne Pepitone CNN.

January 2013.

15. eBay Inc. Reports Strong Fourth Quarter

and Full Year 2012 Results. eBay

Inc. December 2012.